Kyle Inan - Evolution of the International Monetary System

- Название:Evolution of the International Monetary System

- Автор:

- Жанр:

- Издательство:неизвестно

- Год:2021

- ISBN:нет данных

- Рейтинг:

- Избранное:Добавить в избранное

-

Отзывы:

-

Ваша оценка:

Kyle Inan - Evolution of the International Monetary System краткое содержание

Evolution of the International Monetary System - читать онлайн бесплатно ознакомительный отрывок

Интервал:

Закладка:

Kyle Inan

Evolution of the International Monetary System

“A historical analysis of the Classical Gold Standard System, the Inter-War Period, the

Bretton Woods Agreement & the International Monetary Order of the Post-1973 Era”

It is within the purview of this book to analyze the emerging monetary policy trends following the establishment of the Bretton Woods System that brought about the creation of the International Monetary Fund (the IMF) and the International Bank for Reconstruction and Development (IBRD) to assist member countries with restoring their balance-of-payments equilibrium through the enactment of fixed exchange rates currency regime and through credit lending to poor countries in need. The main purpose for introducing these systems was to concretely establish a “par-value” exchange rate among member countries in which they would peg their respective currencies to the U.S. dollar.

Furthermore, the book aims to explain the several important reasons for the failure of the world monetary reform after the collapse of the Bretton Woods System in an era compounded by the problems of shortage of U.S. dollars in the world economy as well as the recurring trade deficits that forced European countries to reconsider their commitment to the fixed exchange rate system. The book explores the reasons that led to the creation of “the European Monetary System (EMS)” as well as the European motives behind creating a single unit of currency, vis-à-vis the “Euro.” It concludes with an overall analysis of the historical evolution of the international monetary system.

The Historical Evolution of the International Monetary System

Since the inception of the social dynamics crisis caused by the Napoleonic Wars until the wake of the Industrial Revolution in the eighteenth century, there was little room for global interaction among states as there was no stimulus to engage in international trade. The absence of a regulatory system around the globe followed by the exploitation of resources in underdeveloped countries by hegemonic powers, laid the foundations for excess capital mobility giving rise to disruptive shocks to the international system.

The lack of a worldwide commercial network and uncontrolled economic activity pushed countries away from the balance-of-payments equilibrium. The prospects for international trade remained relatively low; especially without the existence of institutions capable of supporting markets both at the domestic and international levels.

By the end of the nineteenth century, the unilaterally adjusted monetary statutes of many nations around the world had created a set of conditions for the minting and circulation of two distinct metallic mediums of exchange: gold and silver . Countries that allowed the simultaneous circulation of gold and silver both as acceptable units of currencies in their economies were operating under a system that was known as “bimetallic standards.” At the time, with the exception of Britain and France, almost all of the European countries were operating on silver standards. In essence, Britain had differed from other countries that have previously adopted the silver standard mainly because the British economy had been using gold as the standard currency from the start of the century.

Similarly, France was also an exceptional case in this era since the French monetary laws were representative of bimetallic statutes. However, the privilege of allowing the simultaneous circulation of both gold and silver presented its own challenges.

A significant historical example of this dilemma was during the last years of the nineteenth century when 14.5 ounces of silver were being traded roughly for an ounce of gold in the market place in France.

From time to time, whenever the price of gold in the world market rose more than that of silver’s, let us say up to a point where 15 ounces of silver were being traded in exchange for an ounce of gold, then such a market price of gold would create an incentive for arbitrage. Thus, the arbitrager would have a window of opportunity to be able to import at the previous quantity of “14.5” ounces of silver and have it coined at the mint price. Then initially, that silver coin would be traded in exchange for an ounce of gold and the gold (i.e. the extra half ounce of silver) that the arbitrager had earned in the domestic market would be exported at a cheaper rate and a be sold for 15 ounces of silver on foreign markets.

Ultimately, the arbitrager would continue to export gold and double his earnings insofar as the market ratio had stayed considerably above the mint ratio.

Conversely, if the market ratio were to fell below the mint ratio (i.e. after a few discoveries of new gold reserves) then arbitragers would import gold and export silver. This window of opportunity was called the “ Gresham’s Law ”, where the bad money with a lower commodity value, vis-à-vis silver, would drive out the one with the higher commodity value, vis-à-vis gold.

In the last quarter of the nineteenth century, the shortcomings of the prevailing bimetallic system had divided the Western countries among themselves. This took place especially between those who were operating solely on silver as the only medium of exchange and those who were solely operating on gold as well as those operating on bimetallic standards; on both gold and silver. This situation was causing many of the industrializing European economies to experience growing difficulties in international transactions as well problems in creating a smoothly functioning domestic economy.

As Britain and the United States, two countries that were fully committed to gold, emerged as the world’s most prominent financial and industrial powers with the advent of the industrial revolution by the end of the century, some of the few countries with silver standards have decided to peg their silver coins to the gold standards of those countries. “By the beginning of the twentieth century, there had finally emerged a truly international system based on gold.” (Eichengreen, 2008, pg. 19)

This system was called the “Classical Gold Standard System.”

The Classical Gold Standard System (1880-1914)

“ The breakdown of the international gold standard was the link between the disintegration of world economy since the turn of the century and the transformation of a whole civilization in the thirties.” (Polanyi, The Great Transformation, pg. 20)

Historically, the most famous and durable international monetary system was the Gold Standard System largely because several things have served as a medium of exchange in the early days of the nineteenth century. For instance, some of those things were cattle, sheep, wine, jewelry, and diamonds as well as many other precious stones that were being bought and sold in the markets. However, metal coins had some unique characteristics to be more acceptable; (I) First of all, metal coins were easy to divide (divisibility), (II) Secondly, coins were also very durable (durability), (III) Thirdly, the supply of precious metals such as gold and silver were stable to a great extent, and their final and their most important feature which served in the facilitation of daily transactions (IV) was their recognizability. It is primarily for these reasons that metal coins became the most popular medium of exchange over time driving out others.

In addition to the gold’s ability to serve, as an important medium of exchange, there were also three main rules to the Gold Standard; (i) All countries had to fix the price of gold in terms of their domestic currency. This was called the “mint price of gold.” (ii) Governments had to support the mint price for transactions with the public to assure that the mint price equaled to the market price of gold. Because, in the event the market price is higher (Market Price > Mint Price) than the mint price; then people would buy the gold from the government (i.e. from the Treasury Department of a given country) and the supply of gold in the market would go up while the market price of gold would go down. The opposite of this would happen whenever the market price of gold was lower than the mint price (Market Price < Mint Price). In that case, people would choose to sell the gold to the government and the supply of gold in the market would go down whereas the market price of gold would eventually go up.

A third most striking feature of the Gold Standard System was (iii) the fact that the melting of gold coins was legal. This would assure that the value of gold coins was same for monetary and non-monetary purposes.

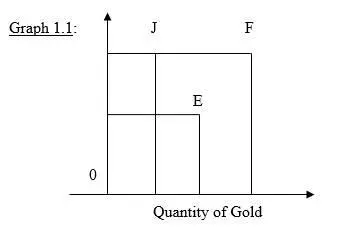

At this point, some of us might inquire about the conditions as well as the factors that determine the value of money supply under the Gold Standard. An illustrative graphical example would help us explain the key determinants of the money supply of gold under this system.

Graph 1.1 shows that, the quantity of gold demanded for non-monetary purposes will go down and the quantity supplied of gold is also expected to increase after an increase in the price of gold. Under the Gold Standard System, the government will fix the mint price above the Po level to assure that there is an adequate supply of gold to make coins out of. At a mint price of Pm , the quantity demanded of gold for monetary purposes is the distance between the origin and point Q1, whereas the quantity supplied of gold equals the distance between the origin and point Q2. In this case, the distance between Q1 and Q2 or the range between points E and F will be the gold used in the making of coins. (i.e. excess supply of gold available for gold coins.)

Under the Gold Standard System, the value of money supply can also shrink or expand based on the demand for gold for non-monetary purposes and the supply of gold. Specifically meaning that shifts in demand for gold for non-monetary purposes or the supply of gold curve can create a change in the money supply.

There are three main reasons that would cause a significant shift in the demand curve. These are as follows: (1) if there is an increase in the income of consumers, (2) if there is a change in the expectations of future prices, and if (3) there is a change in the prices of related goods and services. Since an increase in demand for gold for non-monetary purposes can cause the money supply to decline, if the supply of gold increases after a gold rush (i.e. The U.S. California Gold Rush of 1848-1855) then a shift in the supply of gold curve can also be observed.

To summarize, there are primarily three distinct factors that can cause a shift in the supply of gold curve. The three factors are: (a) If there is an increase in the number of producers; for instance, if new gold mines are discovered. (b) If the cost of production changes; for instance, if transportation becomes cheaper. (c) If there is a considerable change in the technology of production; for instance, it might become easier and less costly to extract gold with newly advanced technology.

Furthermore, a most remarkable feature of the gold standard system was its included benefits at the operational level. For instance, the money supply was independent of any government action mainly because the money supply would grow or expand at the same rate (simultaneously) with the gold supply. If there were no new discoveries of gold, then there would not be an expectation for an increase in the money supply.

Since governments had no control over the money supply under the Gold Standard, due to the aforementioned reasons, they would not be able to arbitrarily print more money and cause inflation. Therefore, there was virtually no possibility of inflation under this system. In other words, this system had promised long-term price stability to its owner, which could be described as its most significant benefit.

Читать дальшеИнтервал:

Закладка: