Коллектив авторов - Money, money circulation and credit

- Название:Money, money circulation and credit

- Автор:

- Жанр:

- Издательство:Казахский национальный университет имени аль-Фараби Литагент

- Год:неизвестен

- ISBN:978-601-04-1569-0

- Рейтинг:

- Избранное:Добавить в избранное

-

Отзывы:

-

Ваша оценка:

Коллектив авторов - Money, money circulation and credit краткое содержание

This еducational manual is published for students and lecturers of the economic universities.

And is also could be useful for credit and fi nancial system employees.

Any distribution of this work or its part without the author’s agreement or other actions which violate a copyright norms are prohibited and punished by law.

В учебном пособии рассматриваются вопросы теории и практики денег, кредита и банковской системы страны, в частности, сущность денег, денежное обращение, кредит, денежная, кредитная и банковская система государства, становление и развитие банковской системы республики, ее функции и операции, развитие рынка ценных бумаг, фондовая биржа и международные валютно-кредитные отношения.

Учебное пособие предназначено для студентов и преподавателей экономических вузов. Также оно может быть полезным работникам кредитно-финансовой системы. Любое распространение этой работы или ее части без согласия автора или других действий, которые нарушают авторское право, запрещены и караются по закону.

Money, money circulation and credit - читать онлайн бесплатно ознакомительный отрывок

Интервал:

Закладка:

Money turnover represents a complex of cash-in-hand flow and cash wire movements. There is a tight fit between them both: money constantly transfers from a cash form into a cashless and otherwise. The correlation of these two constituents changes as settlement relations develop and improve.

With the commodity circulation and settlement relations development the structure of monetary stock and correlation between the cash and cashless spheres of money turnover changes. If to the end of XIX thcentury the cash settlements prevailed in a money turnover of any country but nowadays in the developed countries the vast majority settlements are made in cashless order.

The cashless money circulation prevails which is served by cheques, credit cards by means of transfer of sums against the invoices of banks and savings banks, electronic translations. Thanks to the settlements computerization drawn on the accounts money easily transfers from cashless into cash money circulation. Besides the money turnover is completed by the treasure bills, obligations, certificates which confirm bank inpayments of a definite sum or gold.

The different instruments of the bank current accounts and deposits usage appeared. Among them are credit cards of «now» accounts for payments against the orders of writing off of amounts from saving accounts, of accounts for money transfers to third persons, etc.

1.3.2. Cash-in-hand flow and its organization

Cash-in-hand flow is a cash money movement in the sphere of turnover and its performance of two functions: of the mean of payment and of the mean of circulation. Cash money is used for payments of goods, services and works; for settlements which are not connected with movement of goods and services (payment settlements of salaries, bonuses, allowances, stipends, pensions, their revenues, social payments, for housekeeping needs, for business trips, for representational expenses, for agricultural products purchases, etc.).

The cash money movement is performed by means of different types of money: banknotes, metal coins, other credit instruments (bills of exchange, cheques, credit cards). The emission of cash money is performed by the Central (as a rule State) Bank.

As was mentioned before in Kazakhstan it is the National Bank which issues cash money and withdraws it in case of its worn-out state and changes money onto the new samples of notes and coins either. There are the following normative legal documents which take a control of a cash money circulation in our country:

The board of directors of the National Bank of the Republic of Kazakhstan decision dated from March 3, 2001 № 58 «The regulation of cash and safe deposit transactions conducting in regard to an encashment of banknotes, coins and real values in the second-tier banks and enterprises which perform the separate types of bank transactions of the Republic of Kazakhstan».

The board of directors of the National Bank of the Republic of Kazakhstan decision dated from October 10, 2002 № 401 «The rule of licensing and regulation of activities of an encashment of banknotes, coins and real values of the juridical entities excluding banks».

The board of directors of the National Bank of the Republic of Kazakhstan decision dated from May 28, 2007 № 56 «About the confirmation of an instruction on security and rooms arrangements of the second-tier banks».

The division of cash money onto paper and metal is determined by practical considerations of the money circulation convenience. For example in USA about 10 % of money is considered reasonable to keep in small coins. Consequently bypassing a simplification of settlement mechanism and a tendency to electronic money development the commodity production cannot avoid the cash money usage.

It keeps meaning:

– for disadvantaged population;

– in the conditions of crisis when a quest of cash money increases;

– for an illegal economic activity, evasion of property taxes, because cheques, credit cards, transactions are used by judicial authorities in evidence of different offenses.

Nowadays a retail trading in Kazakhstan basically consists of cash-in-hand flow. The majority of population is not served in banks and paid in cash. The clients who have banking accounts prefer to withdraw cash and use it for all their expenses.

For tax authorities it is almost impossible to trace and control the taxpayers revenues on the markets with cash-in-hand flow domination. The main part of cash money is spent on small purchases. Just according to these small payments on retail trading market the different types of production and import supporters can distribute a considerable volume of an unaccounted goods and the State at that faces a problem of tax collection.

Many people nowadays work without an appropriate registration and as a salary is paid in cash it is quite difficult to collect the taxes between an employer and an employee. Today the state doesn’t have any mechanisms allowing to register a real volume of consumption of the population and estimate a business situation in the sphere of indirect taxation.

The money owner needs a transparency and is forced to count constantly the available sums of money. Thus he prefers to keep it in a wallet. If he could see the rest of sum every time he wants and his money in some manner would secured from inflation thus surely he wouldn’t refuse to keep money in bank and to have an access to it by means of payment cards usage.

The National Bank of Kazakhstan specifies the requirements of cash services organization for banks and their clients and also of cash money holding, shipment and accounting. Under the law of RK dated from June 29, 1998 № 237 («BegoMOCTH napaaMema PK», 1998 № 11-12, article 177) the settlements between the juridical entities on a sum exceeding 4 000 monthly calculation indexes are made only by bank transfers.

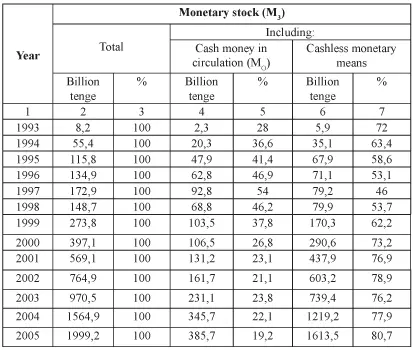

Table2

The structure of monetary stock in the Republic of Kazakhstan *

The data of Table 2 shows that in Kazakhstan the dynamic fluctuation of the monetary stock volume is observed. In the monetary stock total volume the cash money took more than 20 % till 2005. It was related to the economic situation changes in the country while in modern conditions the share of cash money in the total monetary stock volume is not big especially in the industrially developed countries (for example in USA it amounts about 8 %).

Beginning from 2005 the share of cash money in circulation decreases and on 2009 it came to 12,4 % what is very good rate. It improves the structure of monetary turnover, widens the payment cycle and thus the circulation expenses decrease.

There is a tight fit between the cash and noncash circulations: money constantly transfers from one sphere of circulation into the other, it forms a total monetary turnover where the unified money acts.

In the national economic the cashless settlements prevail performed through the banks.

1.3.3. Cashless money turnover and its forms

Cash wire movements is a value transaction without cash money participation. The share of cashless settlements in Kazakhstan on January 1, 2009 takes 88 % of monetary stock. A high level of cashless settlements in any country shows a right and proper organization of the whole money turnover.

A noncash money turnover is performed by means of cashless settlements which are made without the usage of cash money by means of money medium transfers against the invoices in the loan institutions and by means of mutual claims offsets. Such settlements have an important economic value in the turnover acceleration, cash money decrease required for circulation, cost improvement on cash money issue and transportation.

Settlement relations include the following elements:

– the settlements’ members – supplier and consignee, buyer and recipient;

– the objects of settlement transaction (operation) – commodity and material valuables, rendered services, performed works, financial requirements and liabilities and also money and currency resources;

– the authorities which execute the settlements – banking system (commercial banks and cash settlement centres and also clearing agencies);

– the settlement intermediary agents – factoring companies and firms and guarantors either.

In accordance with the banks pattern of participation the settlements are divided onto the extrabank which are made by cosignatories passing the bank, onto the intrabank – between the cosignatories which have their accounts in one bank and onto the interbank which involve the money movement between different commercial banks.

For money medium holding and settlement transaction conducting each business entity opens a settlement / current / credit / deposit or any other account in the commercial bank depending on the enterprise’s status, kind of activity and source of financing.

The principles of cashless settlements were based in the period of credit reform in 1930-1932. The system of cashless settlements which existed in our country from the 30s till 1993 was suited for the costintensive mechanism of economic management and conformed to the administrative command methods of economic management.

Cashless settlements are organized according to a definite system under which the body of principles organization of cashless settlements, demands placed to their organization, determined by the concrete conditions of management and also forms and means of settlements and the involved documents flow are understood.

The first principle of cashless settlements in the market economy environment implies in their performance according to bank accounts opened for clients who’d like to hold and transfer money.

In a competitive business environment a settlements performance via banks should be determined by an economic efficiency, go with economic independence of the market participants and with their activity financial responsibility.

The second principle is that the accounts’ settlements should be conducted by banks to the order of their owners in accordance with determined subordination of payments and within the account balance. This principle includes the market participants’ right of their own determination of payments’ subordination from their accounts. It provides a significant move on the way toward the real economic independence of economic executives’ confirmation.

The main demand placed in this case by bank to market practitioner as a settlement participant is to make payment within the outstanding balance of funds deposited in accounts.

The third principle is a principle of market participants’ free choice of cashless settlements forms and their consolidation in commercial agreements under the banks’ noninterference into the contractual relations. This principle is also directed onto the economic independence confirmation of all the market participants (irrespective of the form of ownership) in the organization of contractual and settlement relations and on their financial responsibility raising for the efficiency of these relations. Bank plays role of a representative in payments.

Recently a tendency of a payer’s transformation into the main subject of payment transaction is observed because in all the forms of cashless settlement the payment initiative is taken by payer. This fact corresponds to the market relations of our country’s economics.

In order to make a cashless settlement and money transfer it is necessary to use a payment instrument by means of which the payment initiates and on the basis of which money transfers.

Читать дальшеИнтервал:

Закладка: